Hi,

We’ve made it to spring! As the season changes, so does the property and lending landscape. Here are four stories making headlines right now:

– Rentals being snapped up

– Houses v units

– Prices surge for new land

– Savings rates above 3% p.a.

Read more below.

But first….

The results of our recent survey

What is the most important quality of a

mortgage broker?

Our thoughts on this survey

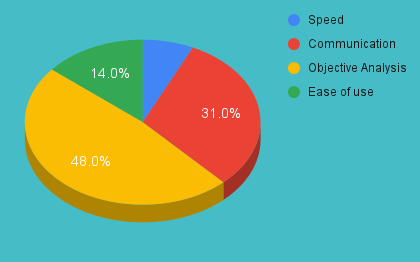

Objectivity – 48%

Objectivity is so important. And, our policy of always being totally transparent allows us to demonstrate our objectivity.

To achieve transparency, we use a filtering process – which we share with you every step of the way:

1. We identify who will lend to you in your circumstances (these days, everyone’s circumstances are different).

2. We then clarify a lender’s willingness and capacity to lend to you with their humans – just to make sure.

3. Only then do we check the rates for those who can and will lend to you.

4. From this rate review, we will give you the short list of these ‘willing and able’ lenders – to get your input via a discussion with us.

5. And only then do we finalise our recommendation.

Communication – 31%

Whilst transparency is key, so is communication.

With your loan, we communicate with you in a number of ways.

1. To save you time and to avoid errors and duplications, we use technology to gather information about you as well as receiving your documents which lenders will need to see.

2. We will regularly ring you, SMS you and email you (and sometimes a combo as we all know how emails, voice mails and even SMSs can be missed or overlooked when we are busy!).

We also follow a 3-day follow-up process – which you can of course vary at any stage (faster or slower). Every 3 days we will reach out to you to make sure you don’t need any help or time to get the next bit done.

Simple to use processes – 14%

Our processes have been designed to be easy to use. However, where you need us to vary our processes to suit you, we will do so! After all, we are here to serve you!

Speed – 7%

Speed is important but speed without Objectivity, Communication and Ease of use is not worth a lot to you. And, dare we say, we know of some brokers who are ‘fast to lodge’ but then have to backtrack when the lender they have chosen says ‘no’.

We see our role as avoiding (or at least minimising) the risk of you receiving a lender No.

And, a quick sample of our free services for you!

Rate Checker

Every year (as a minimum), for our clients with a Variable Rate loan, we will do a rate check for you (if you have a settled loan with us, you will get an email to get this started). We will do the following:

1. Check your rate with your current lender’s best rate for the same product you have.

2. Find a comparative rate for a similar lender with a similar product.

3. Write to your lender or use their online broker portal to request a rate review.

4. And hopefully, we can come back to you with some good news regarding a sharper rate! 😉

It’s a simple process and all you need to do is send us your most recent bank statement and any subsequent rate change advice from your lender.

Property Reports

Via our Free Property Report link www.bir.net.au, investors and homeowners can:

– Order a free property report for a particular property.

– Order a suburb report or a comparison of up to 5 suburbs.

– Access detailed regional reports (over 30 including the capital cities) which include a Property Clock (is it time to buy, hold or sell?).

In September, we updated reports for: Canberra [ACT] < > Launceston [TAS} < > Melbourne [VIC] < > Mackay [QLD] < > Wollongong [NSW] < > Darwin [NT].

Property investors are enjoying strong demand for their rental properties right now, with that demand expected to further increase.

The number of homes available to rent has been trending lower since the pandemic began, with listings in July 2022 31% lower than March 2020, according to realestate.com.au.

As a result, tenants are being forced to compete harder, which is leading to rising rents and lower days on market.

“Australia-wide properties are renting faster than ever, and the number of days it took a rental property to be leased after it was listed on realestate.com.au in July hit a historic low 19 days,” according to the portal.

REA Group senior economist Eleanor Creagh said a “surge” in international student arrivals would add further pressure to tight capital-city rental markets.

“In fact, overseas searches to rent have also skyrocketed in recent months, in the last six months compared to the six months prior overseas rental search volumes are up 59% with the borders having reopened,” she said.

Houses have significantly outperformed units over the past three decades, according to CoreLogic.

During the 30 years to July 2022, median prices increased 453% for houses compared to 307%.

That outperformance occurred in every capital city market:

– Sydney 507% v 340% (houses v units)

– Melbourne 519% v 354%

– Brisbane 390% v 170%

– Perth 325% v 194%

– Adelaide 370% v 289%

– Hobart 423% v 296%

– ACT 431% v 261%

– Darwin 98% v 96%

CoreLogic said the faster rate of growth for house prices was “likely a reflection of the scarcity value of land driving a faster rate of appreciation”.

During the same 30-year period, capital cities (409%) recorded significantly more growth than regional markets (294%).

“The higher growth rate across the capital cities probably reflects a combination of higher demand and greater scarcity of supply compared with regional markets, along with more diversified economic conditions within the capital cities,” according to CoreLogic.

New research by the Housing Industry Association and CoreLogic has found that the supply of new residential land is failing to keep up with demand.

Median lot prices in the March quarter were 19.7% higher than the year before, based on an analysis of 51 housing markets across Australia.

HIA senior economist Nick Ward said this was the strongest annual growth rate since 2004.

“An unusually sharp rise in the price of residential land indicates the supply of land is not keeping up with new demand that has emerged during the pandemic,” he said.

“Constrained supply of land will limit housing activity in greenfield areas from mid-2023 onwards.”

CoreLogic economist Kaytlin Ezzy said the increase in land prices was connected to a reduction in the number of lots sold.

“While increasing interest rates, rising construction costs and increased uncertainty, particularly across the building industry, has likely smothered some land demand, the surge in land prices suggests that those that want to build are finding it difficult to secure lots,” she said.

“With land often taking more than a decade to move through the development pipeline, it’s unlikely we’ll see any material change in land supply for some time.”

Rising interest rates are bad news if you’ve got a home loan. But they’re a blessing if you use savings accounts.

Six banks are now offering ongoing savings rates above 3% p.a., according to a RateCity analysis of the market.

Research director Sally Tindall said if your savings rate is below the cash rate [currently 2.35% p.a.], you’re being taken for a ride.

“There is competition in the market, you just have to get up and look for it. In this environment, a good rate is around 3% p.a., potentially even more,” she said.

How to get an even higher interest rate

If you have a home loan, there’s a way you can earn an even higher interest rate – by depositing money in your offset account.

The money in your offset account reduces the interest-bearing portion of your home loan by the same amount. For example, if you have $500,000 outstanding on your loan and $40,000 in your offset account, you’ll be charged interest on only $460,000 (i.e. $500k minus $40k).

As a result, the return you get on offset deposits is equivalent to your mortgage rate, which will almost certainly be higher than the rate paid by a conventional savings account.